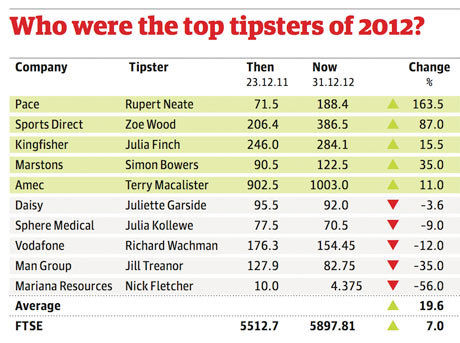

Crisis, what crisis? A late end-of-year surge on the stock market saw investors shrug off worries about the eurozone, a slowdown in China and – a late entrant on the fear index – the US budget impasse. That helped the FTSE 100 to rise 7% since the Guardian's 2012 tips were published.

Crisis, what crisis? A late end-of-year surge on the stock market saw investors shrug off worries about the eurozone, a slowdown in China and – a late entrant on the fear index – the US budget impasse. That helped the FTSE 100 to rise 7% since the Guardian's 2012 tips were published.Happily, our 10 choices did substantially better than the market, jumping by an average of 19.6%.

Pace, the set-top box maker, was the star performer, recovering from disruption caused by a shortage of hard disk drives the previous year. Despite a late wobble when it lost out on an auction to buy Motorola's set-top box business, it soared more than 160%.

Pace, the set-top box maker, was the star performer, recovering from disruption caused by a shortage of hard disk drives the previous year. Despite a late wobble when it lost out on an auction to buy Motorola's set-top box business, it soared more than 160%.Mike Ashley's Sports Direct International climbed 87% after seeing off struggling rival JJB Sports and benefiting from the London Olympics.

Other notable performances came from Marstons and Kingfisher.

There was of course a flop or two, notably Mariana Resources (mea culpa). The gold and silver miner has a supportive shareholder in AngloGold Ashanti, but that did not stop it losing more than half its value. Its Argentinian presence meant it was hit by worries about renationalisation, while there was disappointment at resource levels at its Las Calandrias project.

And so to 2013. The eurozone, the US fiscal cliff and the wider global economy are likely to dominate sentiment once more, so the uncertain atmosphere is likely to continue. With that in mind, we've picked 10 shares we hope will perform well despite market vicissitudes.

Julia Finch

Home Retail Group – Homebase and Argos – has had a rough ride in recent years with shares tumbling from more than 300p to Monday's 126.7p as a result of tough competition, poor sales of computer games and the squeeze facing its less well-off shoppers. It should gain in 2013 from any improvement in the economy and consumer sentiment and from its own three-year turnaround plan. Argos is also one of the UK's most webby retailers, getting 42% of sales online. But there is another factor in its favour this year: the demise of rival Comet, putting its £1bn of annual sales up for grabs. Some 75% of Home Retail's revenues come from Argos, and 51% of Argos revenues come from electricals. If Argos can grab some of Comet's 6% market share to add to its own existing 10% there should be benefits from sales volumes and margins.

Home Retail Group – Homebase and Argos – has had a rough ride in recent years with shares tumbling from more than 300p to Monday's 126.7p as a result of tough competition, poor sales of computer games and the squeeze facing its less well-off shoppers. It should gain in 2013 from any improvement in the economy and consumer sentiment and from its own three-year turnaround plan. Argos is also one of the UK's most webby retailers, getting 42% of sales online. But there is another factor in its favour this year: the demise of rival Comet, putting its £1bn of annual sales up for grabs. Some 75% of Home Retail's revenues come from Argos, and 51% of Argos revenues come from electricals. If Argos can grab some of Comet's 6% market share to add to its own existing 10% there should be benefits from sales volumes and margins.Simon Bowers

Buying opportunities are emerging as US fiscal cliff talks go down to the wire. If you believe the underlying American economy is strengthening, and that the politicians will find a compromise in the national interest, there are plenty of London-listed stocks worth looking at. Drinks group Diageo has a strong exposure to the US market. Shares have had a good run in 2012, but have eased back a shade in recent weeks to £17.87. The company was frustrated in its efforts to take over tequila brand Jose Cuervo and may only play a marginal role, if any, in the bidding war for US rival Beam next year. That may be no bad thing for the share price. Diageo does have exposures to some of the toughest European economies, but its global reach ought to mean continuing difficulties here are absorbed. The acquisition of a majority stake in India's United Spirits group will complete next year. It is just the latest development in Diageo's push into the fast-developing Bric markets.

Buying opportunities are emerging as US fiscal cliff talks go down to the wire. If you believe the underlying American economy is strengthening, and that the politicians will find a compromise in the national interest, there are plenty of London-listed stocks worth looking at. Drinks group Diageo has a strong exposure to the US market. Shares have had a good run in 2012, but have eased back a shade in recent weeks to £17.87. The company was frustrated in its efforts to take over tequila brand Jose Cuervo and may only play a marginal role, if any, in the bidding war for US rival Beam next year. That may be no bad thing for the share price. Diageo does have exposures to some of the toughest European economies, but its global reach ought to mean continuing difficulties here are absorbed. The acquisition of a majority stake in India's United Spirits group will complete next year. It is just the latest development in Diageo's push into the fast-developing Bric markets.Simon Goodley

Betfair chronically mis-priced its 2010 flotation when the betting exchange managed to persuade enough mugs to take a punt at £13 a share. They are just over half that level now, at 686.5p, but despite there being few signs of life in the shares, the company has at least started to acknowledge previous mistakes. New chief executive Breon Corcoran, who was poached from rival Paddy Power, has started in a pragmatic mood, withdrawing from costly foreign adventures such as in Germany, where the company is struggling to foresee a future regulatory and tax regime that will allow it to make a profit. He's also retreated from vanity projects such as the company's financial betting exchange, LMAX. As both of these areas were once used to justify the Betfair float price, critics might argue that the moves make the company look unambitious. But industry insiders reckon that Corcoran has plenty of early easy wins to focus on, principally by cutting Betfair's cost base to swiftly increase profits. After more than two years as a public company, this might finally be the time to bet on Betfair.

Betfair chronically mis-priced its 2010 flotation when the betting exchange managed to persuade enough mugs to take a punt at £13 a share. They are just over half that level now, at 686.5p, but despite there being few signs of life in the shares, the company has at least started to acknowledge previous mistakes. New chief executive Breon Corcoran, who was poached from rival Paddy Power, has started in a pragmatic mood, withdrawing from costly foreign adventures such as in Germany, where the company is struggling to foresee a future regulatory and tax regime that will allow it to make a profit. He's also retreated from vanity projects such as the company's financial betting exchange, LMAX. As both of these areas were once used to justify the Betfair float price, critics might argue that the moves make the company look unambitious. But industry insiders reckon that Corcoran has plenty of early easy wins to focus on, principally by cutting Betfair's cost base to swiftly increase profits. After more than two years as a public company, this might finally be the time to bet on Betfair.Jill Treanor

2012 was not a good year to have tipped Man Group, the world's biggest listed hedge fund group, which relies on its "black box" AHL flagship fund for its performance. AHL, which uses computers to spot trends in markets, has been blown off course by quantitative easing and Man's shares had fallen almost 80% since the start of 2011. Yet as 2012 drew to a close, the shares started to perk up after chief executive Peter Clarke was shown the door. Installing Manny Roman, who arrived with the acquisition of hedge fund GLC, has given investors fresh hope, while new finance director Jonathan Sorrell – son of WPP boss Sir Martin Sorrell – is expected to start cutting costs. With a bit of luck, the shares – now 82.75p – will recoup their 2012 losses during 2013.

2012 was not a good year to have tipped Man Group, the world's biggest listed hedge fund group, which relies on its "black box" AHL flagship fund for its performance. AHL, which uses computers to spot trends in markets, has been blown off course by quantitative easing and Man's shares had fallen almost 80% since the start of 2011. Yet as 2012 drew to a close, the shares started to perk up after chief executive Peter Clarke was shown the door. Installing Manny Roman, who arrived with the acquisition of hedge fund GLC, has given investors fresh hope, while new finance director Jonathan Sorrell – son of WPP boss Sir Martin Sorrell – is expected to start cutting costs. With a bit of luck, the shares – now 82.75p – will recoup their 2012 losses during 2013.Nick Fletcher

Issuing a profit warning in the middle of a takeover situation is not ideal, and defence group Chemring duly suffered the consequences. Its share price collapsed, losing almost half its value over 2012, but even the prospect of a bargain-basement price was not enough to tempt potential bidder Carlyle Group to take the plunge. Chemring replaced its chief executive, and the new man, Mark Papworth, who did well at oil services business Wood Group, will outline his strategy in January. Defence spending in the UK and US is likely to remain under pressure but Chemring now has a platform for recovery. Some excitable souls even believe another bid could eventually emerge, if not from Carlyle then from another private equity group. A speculative bet at 229.6p on Papworth turning things round.

Nils Pratley

Think of this – Ruffer Investment Company – as an anti share tip. It is chosen to provide protection in the rainy investment weather that 2013 may bring. Jonathan Ruffer has positioned the investment trust for a tipping point, the moment when central banks' huge injections of newly created money make themselves felt. He is far from being a hyper-inflation nutter; he's just making the reasonable point that investors need to watch their backs in an era when the US Federal Reserve is openly pursuing reflation to create jobs. The fund, currently at 199.25p, is flush with index-linked government debt, gold and Japanese equities. It ain't glamorous. But, one day, those assets could be the right place to be. Is that year 2013? Ruffer is often too early in his calls, so who knows? But surely you don't expect guaranteed winners from newspapers' share tips.

Think of this – Ruffer Investment Company – as an anti share tip. It is chosen to provide protection in the rainy investment weather that 2013 may bring. Jonathan Ruffer has positioned the investment trust for a tipping point, the moment when central banks' huge injections of newly created money make themselves felt. He is far from being a hyper-inflation nutter; he's just making the reasonable point that investors need to watch their backs in an era when the US Federal Reserve is openly pursuing reflation to create jobs. The fund, currently at 199.25p, is flush with index-linked government debt, gold and Japanese equities. It ain't glamorous. But, one day, those assets could be the right place to be. Is that year 2013? Ruffer is often too early in his calls, so who knows? But surely you don't expect guaranteed winners from newspapers' share tips.Terry Macalister

Some online companies are in the sin bin over tax issues but Asos, with its logistics base at Barnsley in the white rose county of Yorkshire, continues to smell sweetly. The net-based fashion retailer was also heading for a "stonking Christmas," according to its chief executive and founder, Nick Robertson, and there are reasons to believe its already highly valued shares, £26.91, should still find more uplift next year, too. New international sales helped drive up profits 40% in the 12 months to 31 August, and there are high hopes for a forthcoming move into the Chinese and Russian youth markets.Simon Neville

When SSE – Scottish and Southern Energy as was – announced a 38% boost in half-year profits in November while simultaneously raising gas and electricity prices, people were quite rightly fuming. So if you can't beat them, why not join them? 2013 for SSE is likely to see more of the same – profits continuing to rise. Throw in a dividend yield of more than 6% and you're unlikely to find a better return on such a safe investment. Confusion on Britain's energy future remains, depressing SSE's share price a little, so as we inch each day closer towards the government being forced into making a decision over the country's needs, expect a nice boost to the current £14.18. And with outspoken chief executive Ian Marchant at the helm, SSE has the best chance of getting its own way.Juliette Garside

TalkTalk shares are up 70% to 233.6p since January, but chief executive Dido Harding (pictured below), is only just getting going: the rollout of TalkTalk's budget pay TV service, along with fibre broadband and mobile phone deals, began in earnest in November. The model has worked well for Virgin Media and BSkyB: increase profits by selling more services to your existing customers. But TalkTalk should be able to grow headcount by tapping into Freeview's 10m users. Some of the potential is already priced in, but Goldman Sachs has a 290p target by November next year, underpinned by healthy dividend growth.Rupert Neate

When one of the world's best-known activist investors declares he's made it his "patriotic" duty to destroy a company, there's probably something in it. The market certainly reckons Bill Ackman's on to something with his $20m bet against slimming powder and body-building supplement company Herbalife – the shares fell 38% last week when Ackman revealed his short position and accused the company of being "the best-managed pyramid scheme in the history of the world". Ackman, founder and chief executive of hedge fund Pershing Square Capital Management, told investors he was more committed to bringing down Herbalife "than any investment I have ever made, full stop". Herbalife denies all the accusations. Although shares have already fallen to $29.39, Ackman says: "Our target price is zero, because we think the business will fail." If you can get your hands on any to short (it might be quite tricky; Ackman's shorting as many as he can), you might profit from Herbalife's decline. Ackman's committed to giving all profits to charity (you don't have to).

No comments:

Post a Comment